We bought a house! We’re moving in tomorrow and couldn’t be happier.

We started house hunting in March and walked through more than 100 houses before finding this really great one. It was a long, frustrating process and I hope to never need this information again, but perhaps you'll find it useful.

We started off getting a general idea of what we could afford by looking at our budget and how much we could spend per month on mortgage, taxes, and insurance. I played with the Quicken Loans Mortgage Calculator mobile app a LOT over the last three months, and got an idea from that on how much house our monthly budget meant. It seemed to us that the industry really doesn't look at the numbers that way. They do it backwards. They look at your overall income - not your take home pay - and then calculate a house value. I can't imagine why that's a good idea for the buyer, but we quickly got the impression that nothing in the mortgage industry is intended to be good for anyone but the banks. (*cough cough* mortagecrisisain'tfixedyet *cough* Oh, excuse me)

Anyway, we got an idea from the Quicken app of what we could afford and what we could be preapproved for. We could've been approved for more house than we could actually afford, but didn't want that. We like eating out, we like our cell phones, we like fast internet and we like not pinching pennies. Our theory was that if we can't afford a house and our current lifestyle, then we can't afford the house. I'd much rather shrink our budget and pinch pennies when a pipe bursts, than to have a pipe burst when we've already shrunk our budget and have to live off credit cards to pay for the repairs. However, I also really like adorable little craftsman houses, and had to figure about what price range we'd find a forever home within. Luckily, they both lined up pretty well - in March at least.

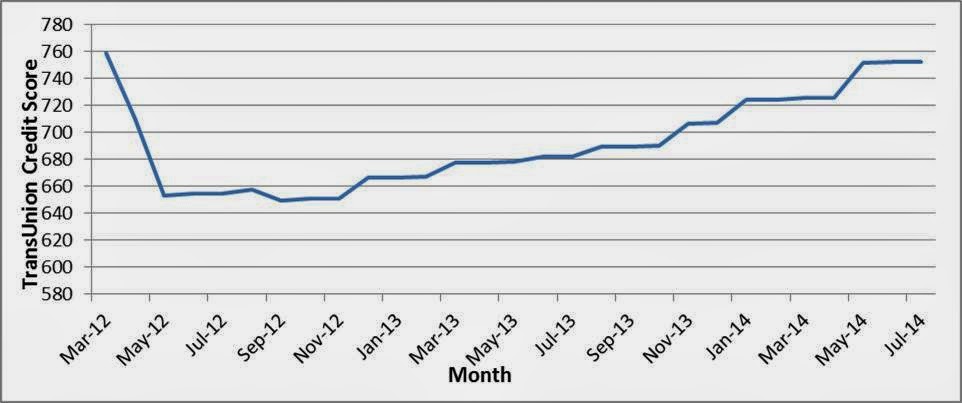

We only used Corey's income to qualify for the mortgage. My credit score and credit report would've significantly increased our interest rate, if not had us denied entirely. None of them minded only using Corey's, or even batted an eye. I can't imagine how much money the banks would've pretended we could afford if they'd actually looked at both our incomes. Something ridiculous that would've meant nothing but ramen for five years. But now that I’m more than a year passed my first missed payment on the mortgage, here’s how my credit is shaping up:

I don't know if my zero missed payments is an error, or if having the mortgage "closed as agreed" meant the missed payments got wiped out. I decided not to investigate. :) I had expected that the foreclosure would've shown up as a "derogatory mark" but still nothing.

Back on the house hunt, we'd only gone to a handful of open houses before finding an agent we liked at one and decided to work with her. She recommended we immediately get formal pre-approvals. So in early April, we talked to Quicken, Wells Fargo, and a mortgage broker she recommended, and requested they pre-approve us for the amount I had planned. They did all tell us we could get approved for more, but we didn't want it. It felt a little like feeding in to the slimey mortgage industry to let them tell me my own budget. Also on the recommendation of the agent, if your preapproval letter says you can afford $50,000 more than what you bid a house, a seller will know you can afford to raise your offer. We were happy with our pre-planned amount.

Now we had pre-approval letters in hand, we had an agent to show us through houses, and I had a real estate mobile apps to show me every single house in our neighborhoods and price range. Weekend after weekend after weekend, we'd tour about 10 houses, and a handful more on weekday evenings. We saw lots of diamond-in-the-rough houses that we couldn't afford to make amazing, but saw the potential. Saw lots of cute tiny houses that we could've bought if we wanted to just jump in the market and sell it again in a few years. But that's what I did with the condo, and look how great that turned out... We decidedly did NOT want a place as an "investment." Houses are a terrible investment. Your money is tied up unless the market happens to decide you have equity today. You pay twice the price because of interest, and you could lose it all in one big Seattle earthquake. So no investment-based decisions! We wanted a home that we'd be proud of and want to stay in forever, even if we end up underwater on it in the future.

Interstingly, we found that we were very much the demographic at most open houses we went to. The other couples looked like us, were all late twenties to mid-thirties, and clearly had similar incomes if they could afford the same houses and neighborhoods as us. We didn't see very many people with kids even. The rest of the people at open houses were very contractor-y looking, scooping up the investment properties.

At the very end of April, we found one! It was pretty great. Kitchen was a little small, and one less bedroom than we wanted, but it had great updates and some unfinished basement space that we could make in to a bedroom if we needed. We even played with Floorplanner.com after taking some dimensions, and figured out exactly how we'd set up our computer desks and tv. We put in an offer well over asking, with a really big earnest money check, with a letter of how much we love the place, with an escalation clause saying we'd go another big amount over if anybody beat our first offer, and with no inspection contingency because we'd already had an inspection done. Our agent was sure we'd need all five of those. She'd recently seen houses with more than a dozen offers, and anybody with an inspection contingency still in their offer would be ignored. Apparently, the housing industry is roaring again in Seattle.

But we didn't get it. It sold for about $60,000 over asking with eight offers in under a week. It was clearly underpriced but we didn’t think by THAT much.

After that, it was May, and we returned to weekend after weekend after weekend of more houses, more disappointments, lowering expectations, the same homes becoming too expensive for us, and a shrinking buying power. Interest rates were creeping up, so we couldn't look at as much house, plus we had to account for a larger margin beyond asking price to beat out other buyers. We found one that Corey really liked, and met all our on-paper needs, but I just didn't like it and couldn't explain why. That was tough to pass up. (It ended up selling for $30,000 over our max budget, so we'd never have gotten it anyway) We found a few that the agent loved, and also met our on-paper needs, but didn't really appeal to either of us. I was sure I didn't want to increase our location options though. I don't need a big house, so there's no reason to go to the suburbs just so I can get a big house. Location, location, location.

By June, we were starting to really consider buying a more temporary house and selling it in a few years. But then, we found it. :) It listed on a Thursday, we saw it Saturday, went back Sunday with Corey's parents to the open house, got an inspection done Monday morning, and made the offer Monday afternoon. By Monday night, we'd bought a house!

It didn't have very good listing photos, and didn't have any furniture to show you the size of each room, so wasn't one to really draw you in based on the pictures. But when we got in it, the floor plan was great. It's a 60 year old house, but they'd just finished a major renovation on it so everything was new. Being mid-century instead of turn-of-the-century has its perks too, even if it's not quite the same charm as a craftsman. It had an addition at some point so has a great living room in the back that is uncommon for the age and location. It had more than we were expecting: a full laundry room that could really be a bedroom if we ever need another, an attached garage and shop, and carports with a second shop off a back alley, a big kitchen, lots of windows. They'd put a lot of work in to it, and yet, nobody but us really came. We didn't see anyone else drive by the house while we were there (uncommon), didn't have any other agents walking people through (also a bit uncommon), and didn't even see a single other person at the open house (very uncommon).We bid only $1000 over asking based on how little competition there appeared to be, but with another escalation clause, another letter on how much we loved it, another large earnest money check, and the inspection already done.

Not a single other offer came in, and they even pushed back the cutoff for bids by a few hours, hoping more would come. I think just having the bad listing photos turned people off and this house was destined to be ours.

By Tuesday, we were talking again to Quicken, Wells Fargo, and the mortgage broker, and this is where we made our only real mistake. I knew our next step was to get "good faith estimates" from every lender, so Corey went and asked all of them for one by the next day. Apparently, that's not what we should've done at all, because we got a jumble of answers. One just refused to do it - "I can't do that in a day". One got us a pretty close approximation with some disclaimers. And one sent us three different estimates showing different points. ("Points" mean buying down the interest rate. I pay the bank a fee, and they lower the interest rate by a smidge. You can also have the bank pay you and they raise the interest a smidge.) The two equivalent offers - no points - were about the same. One had a little lower closing costs, one had a little lower interest rate. We didn't have the capital for any points, so were just comparing the base values. I was also obsessed with getting the lowest interest possible, so wasn't going to let the bank pay me a pittance to rip me off over 30 years.

Apparently, what we SHOULD'VE done was asked each of them for the good faith estimate on the HUD-1 form. This is a government regulated form that they're required to give you at closing. And by asking for a good faith estimate, we thought we'd be getting it on one of these forms. Not a single one of them told us the much more reasonable answer of "A real good faith estimate takes 4-5 days. If you'd like something today, I can't provide it on the HUD-1 but I could get you a rough estimate". Of course, it would've been way smarter of us to have let them all take a few days to get a real estimate on a standardized form so we could actually compare every entry on the form from all three lenders, but we didn't know. So, our ignorance, and no one telling us otherwise, may have led to us paying more in interest and closing costs than we could've otherwise. I had wanted to take the good faith estimates from two places, show them to the third, and ask for them to match or beat the other two. It was my brilliant plan. But we got such a jumble of garbage that it was hopeless. Next time, HUD-1 estimate or we don't work with you.

We ended up picking the mortgage broker over either Quicken or Wells Fargo. He had the lowest interest, and even if his closing costs were higher than the other guys, we just plain liked him better. He'd been helpful, answered our questions, was local, and replied quickly to everything. He also is well experienced with our agent and with the local filing requirements, so having them all familiar with each other meant a smoother closing, we learned later. If we'd have gotten HUD-1s from everyone, we'd have shown them all to him and had him match it so that he could be the one we did the loan with. Since he's just a broker, he's already sold the loan to a bank, but it ended up being a local bank, not national, and we're really happy we chose him.

After officially picking the broker for our loan, we talked to our insurance company to get the home insurance set up, we went back to the house a few times to take every dimension in the place so we could play with Floorplanner.com again, and to let my dad do his own inspection and approval. An appraiser went out near the end of the waiting period, and reported that it's actually worth $4000 more than we're paying - excellent. In general though, we twiddled our thumbs impatiently for five weeks, with a few short bursts of activity interspersed.

We did find that my name can be on the title, even if I'm not on the mortgage. The title people don't care what the mortgage says, so that was nice.

We had one odd hitch though. The lender is mandated to have access to our taxes returns for the last couple years. Since we file jointly, that includes me. He said they don't actually use it, but they have to get our permission to access it anyway. Looking at my taxes right now could've really messed up our loan because I have two arguments with the IRS going on right now. On my 2011 returns, I had prepaid half my First Time Home Buyers Credit, thinking I'd owe it all when I foreclosed. I learned later that I didn't actually owe it because I took a loss on the foreclosure, so filed an amendment with the IRS to get my money back. They sent me back a letter requesting the forms again, so I sent them again, but that's been ages now and I still haven't heard anything. I've already spent hours on hold with the IRS over the foreclosure, so am not looking forward to doing it again. The other argument is that they think I owe more for my 2012 taxes. They want one last $500 installment for 2012 on the same First Time Home Buyers Credit, despite the fact that the 5405 form clearly says "you do not have to repay the credit" if you take a loss on the sale/foreclosure. They keep sending me the bill and I keep sending them back the form that says I don't owe them. I met with the Bellevue IRS office, and even though they didn't have any authority to make the situation right, they did at least agree with me that I don't owe it. So if they're trying to get a final payment from you too, don't let them!

Anyway, we’re fully packed and are awaiting the arrival of the moving truck tomorrow morning. My credit is repairing itself slowly but surely. I’m about 30 points above my lowest already, and am still about 80 points below my starting score, but ideally I won’t need credit for a long time yet. There are still some people that disapprove, but it doesn’t bother me. This was absolutely the right choice for me and Corey.

It's all been worth it.

- Jane

{kind=link}