Now that I’ve firmly settled in to this foreclosure plan,

and am working towards it, my mind apparently needed something else to obsess

about. It settled on… Credit!

Knowing that my credit score will be taking a tumble very

shortly, I decided to start investigating how to keep it moderately afloat

during the next seven years as best I could. There’s already room to improve my

credit score, so my next plan of action is to use up as much of that room as I

can.

The place to start my investigation was at

AnnualCreditReport.com to get my credit report. There are plenty of other

websites that all offer to give you your credit report and/or credit score for

free, but this is the one that doesn’t make you sign up for emails, or scams,

or charge a hidden monthly fee. You can do this once per year per credit

reporting agency. I know that I will be very interested in watching my credit

report over the next year, so I decided to only get my TransUnion report. This

means I can check another agency in 4 months, the third in 8 months, and be

back to TransUnion this time next year. I even set a reminder on my calendar at

work to tell me when to check them.

I didn’t see how to get my credit score for free from

TransUnion, just how to see it for “free*” which doesn’t count. I decided I

didn’t actually care what my score was because I could verify that everything

was accurate on my report and because how they do their calculations is beyond

me anyway.

Instead, I spent a bunch of time learning what I could from

ClarkHoward.com. He recommended CreditKarma.com to evaluate my credit report.

(I know, I’m linking a million websites this time. Sorry!) Credit Karma uses

your TransUnion report only, which isn’t ideal, but is better than nothing, and

I luckily had my TransUnion report already in hand, meaning I could verify

their accuracy.

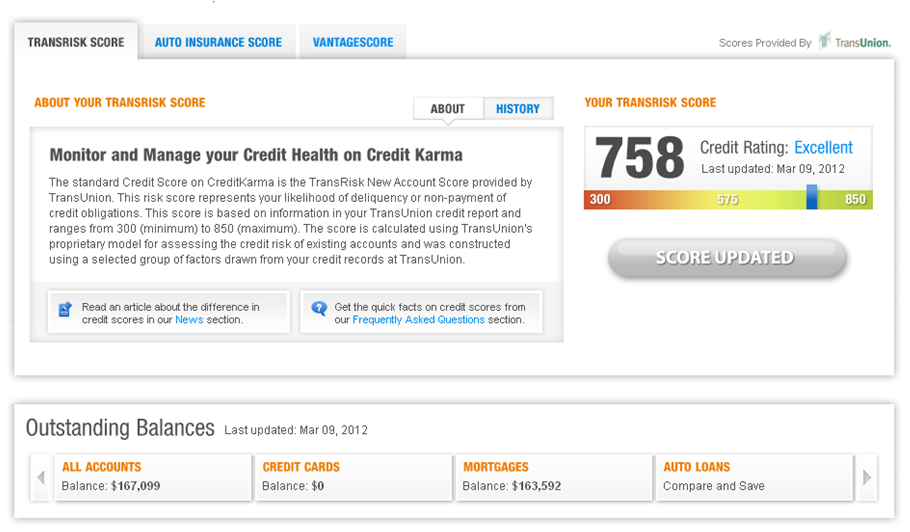

Here’s what Credit Karma had for me:

I’ve got a pretty darn good credit score, but not perfect.

It can see my two loans: $164k for the

condo, and $3500 left in student loans. I did have to give them my email

address and access to my credit report to get this information. And I’m sure

I’ll be getting more spam email soon. They’ve also got a TON of ads once you’re

in there, trying to “save” you money.

The best part of this website, though, and what I really

wanted to use it for, was the “credit report card”. Here’s mine:

And the best part:

It looks like I’m doing great paying on time, having no hard

credit inquires lately, and having no derogatory marks. All of these will be

ruined soon. I’m going to stop paying my mortgage on time, and that will be

reported as soon as Day 30. That will lead to foreclosure, a definite

derogatory mark. Lastly, in order to boost up my other grades, I plan to open

at least one new credit card so I will have at least one new hard inquiry.

Since all of these will be dropping, it’d be wise to try to

improve my other areas so that my score doesn’t have to fall so far. I might as

well take all the hits together while I’ve got lots of time to recover.

This report card has taught me:

1) I

have to start using the one credit card I do have to improve my “C – N/A”

rating in the usage category. Clark Howard says 10% or less is optimum. So

perhaps I’ll switch one monthly bill over to the credit card I already have and

pay it off each month. As long as I use it once every six months minimum, it’ll

stay “active” and helpful to me.

2) I

can’t help the average age of my current accounts, or the C rating. In fact,

it’s only going to get worse by opening up a new line of credit. But, that one

will fix itself in time.

3) I

need to open more accounts! This is not a good idea for everyone. But, my 10

whole accounts is somehow freakishly low. I thought 10 was kind of a lot. The

only way I even got that many was through my student loans and mortgage being

sold a few times each. I should try to get new cards sooner than later, while

I’m better able to qualify for a high credit limit (only got a few weeks left

on that!), and then actually use them.

Thus, my task ahead is clear. Very soon, I will be applying

for one or two more credit cards (more than that seems like too many to juggle

however great my score would be or however many awesome rewards they promise),

and creating some system to use them regularly to bolster my low grades.

Credit Karma had one more gem for me. They’ve got a “Credit

Simulator.” It looks at your credit report then estimates what might happen to

your credit score if you do some things differently.

For example, I asked it what would happen to my credit score

if I open up these two new credit cards with say $20,000 of credit between

them, and have two necessary hard checks against my report. It says my score

will go from 758 to 760. Up is good! Sure, it’s only two points, but it’s up.

It’ll increase my credit limit (thus reducing my usage percentage), increase my

number of credit lines, but also increase the number of checks against the

report. Despite that downer, it nets positive.

Next I asked it what happens to my score if one of my lines

of credit (mortgage) goes to 90 days past due – its longest option. It spits out: 758 to 650. Ouch. Oddly, just

adding a foreclosure to my “public record” only dropped my score to 710. And

very oddly, having one account 90 days past due AND having a foreclosure on the

record only left me with a credit score of 683 - higher than the 90 days only.

Something’s not quite right with this system. That doesn’t

seem reasonable at all. Other places report more like 150 points lost for

having a foreclosure. And the higher your score beforehand, the more you lose.

Now that I’ve got this handy tool though, I’ll be able to

actually to track what does really happen to my credit score. I plan to check

Credit Karma regularly and make a lovely Excel chart of its results. (I like

charts.) Once the bank starts reporting something, and my score/report start

moving, I’ll post it for you to see.

- Jane

No comments:

Post a Comment